Currently, the global upstream landscape in 2025 undergoes a fundamental structural transformation. Specifically, senior leaders now pivot from high-impact frontier exploration toward the meticulous optimisation of mature basins. Consequently, this strategic reorientation responds to macroeconomic volatility and the urgent need for energy security. Companies now prioritise ‘advantaged barrels’. These hydrocarbons offer low cost, short cycle times, and reduced carbon intensity.

Furthermore, stratigraphic traps represent a central component of this transition. These traps contain an estimated 50% of the remaining undiscovered resources in mature provinces like the United Kingdom Continental Shelf (UKCS). In the past, initial exploration phases targeted traditional structural closures. In contrast, subtle lithological variations and unconformities define stratigraphic traps. Therefore, these features demand higher technological precision and integrated subsurface understanding.

The Strategic Reorientation of Global Upstream Portfolios

Moreover, global majors currently employ a dual-track strategy. Leading operators continue to pursue selective frontier opportunities in deepwater Brazil and Africa. Simultaneously, these firms push aggressively for infrastructure-led exploration (ILX) and brownfield revitalisation. This shift responds to shrinking conventional volumes. Notably, markets now reward capital discipline and the maximisation of existing asset lifecycles.

Indeed, mature basin strategies focus on finding the most efficient molecules. Specifically, global oil reserves grew by approximately 16 billion barrels in 2025. This increase brought the total to 1,773 billion barrels by the end of the year. Notably, this expansion resulted from technological advancement and financial optimisation rather than new basin discoveries. As commodity prices stabilised, previously uneconomic deposits became commercially viable assets.

Furthermore, data indicates sustained demand growth, particularly from emerging Asia-Pacific markets. This provides the economic justification for continued investment in mature basins. However, the industry faces transition risks. Specifically, carbon pricing and competition from renewables require new developments to be highly efficient.

Geological Complexity: The Challenge of the Stratigraphic Trap

The exhaustion of structural prospects creates a technical hurdle in mature basins. For instance, interpreters’ image and map structural traps easily using conventional seismic techniques. In contrast, stratigraphic traps occur when lateral facies changes or unconformities trap hydrocarbons.

The Subtle Nature of Stratigraphic Seals

Stratigraphic traps are difficult to identify. Specifically, they often bypass detection on simple top-reservoir depth contour maps. Discovery requires a deep understanding of depositional systems and facies transitions. In pinch-out traps, reservoir quality degrades gradually into a seal. Consequently, this creates drilling risk. For example, a well drilled too far updip may miss the reservoir entirely. Conversely, a well drilled too low may encounter only water.

However, success rates for stratigraphic traps in clastic reservoirs can match structural traps in certain basins. In mature areas, stratigraphic discoveries often deliver larger volumes. This occurs because structural prospects have faced decades of systematic drilling.

Integration of Geological and Reservoir Data

Consequently, success in exploits requires the integration of geology, geophysics, and reservoir engineering. For example, recent activity in Egypt’s Western Desert demonstrates this potential. In 2025, the North Lotus Deep-1 and Arcadia-28 wells showed how re-interpreting older seismic data identifies bypassed pay zones.

Furthermore, the Daenerys discovery validates geologic models for sub-salt Miocene reservoirs. Notably, Talos Energy completed the operation 12 days ahead of schedule. This saved approximately $16 million against the projected budget.

Technological Frontiers in Subsurface Imaging and AI

Additionally, advanced seismic imaging and Artificial Intelligence (AI) revolutionise our ability to resolve stratigraphic features. Notably, the industry has moved beyond traditional attribute analysis. It has entered the realm of high-frequency seismic and Full Waveform Inversion (FWI).

Seismic Foundation Models and Automated Interpretation

Moreover, pretrained seismic foundation models (FMs) emerged as a major shift in 2025. These models, such as PRISM, use self-supervised learning on massive datasets. Once trained, FMs assist with stratigraphic mapping, fault detection, and seismic conditioning. Therefore, this reduces manual workloads and improves interpretation consistency.

Notably, linking these models with Large Language Models (LLMs) allows geophysicists to interact with seismic volumes using natural language. This multimodal approach helps bridge the gap between geophysical data and geological reasoning.

Advanced Imaging for Complex Overburdens

Many stratigraphic traps reside beneath salt or basalt that scatters seismic energy. Consequently, operators now deploy:

- Ocean-Bottom Node (OBN) Surveys: These provide full-azimuth coverage to illuminate sub-salt targets.

- Joint-Domain Full Waveform Inversion: This addresses ‘cycle-skipping’ in complex structures. It delivers more accurate velocity models than conventional FWI.

- 4D Seismic Monitoring: Time-lapse seismic monitors dynamic reservoir changes. Notably, it identifies bypassed oil in compartmentalised stratigraphic reservoirs.

Commercial Risk in Late-Life Asset Development

However, mature basin developments face daunting commercial risks. These include declining production, rising operating expenditures (OPEX), and decommissioning burdens.

The Impact of Fiscal Volatility: The UK Case Study

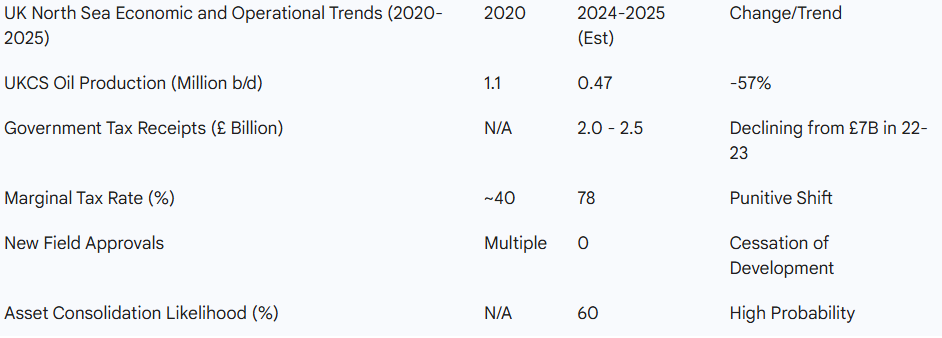

Specifically, the UK North Sea (UKCS) demonstrates how fiscal policy influences activity. The Energy Profits Levy (EPL) raised the marginal tax rate to 78%. Consequently, no new field developments received approval in 2024 and 2025. Notably, UKCS oil production fell to 474,000 barrels per day by September 2025. This represents a 57% contraction over five years.

Indeed, punitive tax environments create a self-limiting cycle. Investment withdrawal accelerates production decline, which shrinks the tax base. Consequently, tax receipts from the sector could drop to £0.3 billion by 2030-31.

Managing Reservoir Compartmentalisation and Late-Life OPEX

Moreover, stratigraphic complexity often causes reservoir compartmentalisation. This leaves stranded oil pockets that existing wells cannot drain. Therefore, operators now employ low-cost well interventions to manage this. Specifically, the NSTA’s 2025 Wells Insights Report notes that interventions delivered 37.5 million boe in 2024. Notably, costs fell from £11 to £9.60 per barrel year-on-year.

Furthermore, late-life optimisation technologies include:

- AI-Driven Well Planning: Reducing non-productive time (NPT) and optimising placement.

- Subsea Gas Compression: Maintaining reservoir drawdown to enhance production in satellite fields.

- Wireless Downhole Surveillance: Providing real-time pressure data without expensive workovers.

The Role of Infrastructure in the Energy Transition

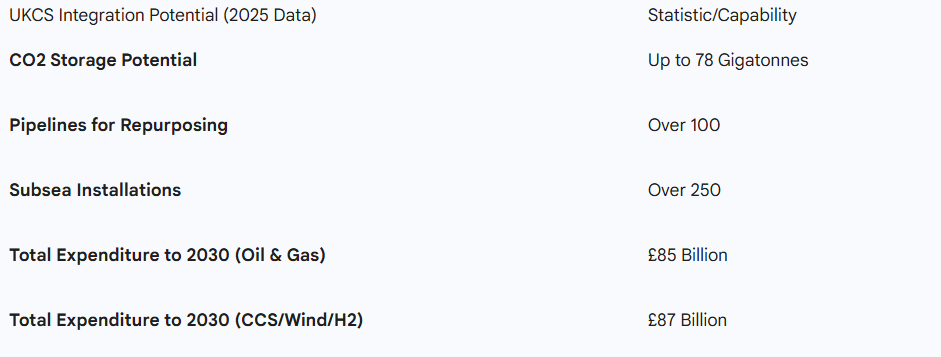

Furthermore, a critical strategic shift in 2025 involves repurposing mature infrastructure. This supports the energy transition. Specifically, late-life assets now serve as platforms for Carbon Capture, Utilisation, and Storage (CCUS).

Notably, the oil and gas sector accounted for 75% of global CCUS capacity in 2024. Repurposing pipelines for CO2 storage offers a pathway to decarbonise operations while maintaining asset value. Consequently, the NSTA awarded the first carbon storage permits for the Northern Endurance project in 2025. This project aims to store up to 100 million tonnes of CO2.

Market Dynamics and the ‘Energy Dominance’ Paradigm

Moreover, the second Trump administration signals a return to ‘energy dominance’. It prioritises increased production and deregulation. Specifically, policy shifts include lifting the LNG export pause and expanding development on federal lands. The U.S. government even created a National Energy Dominance Council in 2025.

In contrast, geopolitical volatility persists. For instance, tensions in the Middle East and the conflict in Ukraine maintain an elevated risk premium. Furthermore, China’s oil demand shows structural changes. Demand for petrochemical feedstocks rises, but transport fuel demand declines due to the expansion of electric vehicle fleets.

Strategic Implications for Senior Upstream Professionals

Ultimately, the stratigraphic era of mature basins offers vast potential. Senior professionals should focus on these priorities:

- Investment in Digital Foundations: Reserve replacement now requires mastery of AI-driven interpretation and foundation models.

- Prioritising ‘Advantaged Barrels’: Focus capital on projects with short cycle times and low carbon intensity.

- Active Portfolio Management: Operators must pool assets or divest non-core holdings in high-tax environments.

- Integrated Transition Planning: Pivot mature reservoirs from hydrocarbon production to CO2 storage to maintain asset valuation.

- Methane Mitigation: Reducing Scope 1 and 2 emissions is a commercial necessity. Notably, Occidental Petroleum (Oxy) successfully lowered its emissions intensity by 11.15% in 2024 through facility consolidation.

In summary, success in this domain requires a focus on data integrity and strategic agility. Senior leaders must view subsurface complexity not as a barrier, but as a competitive advantage.

Frequently Asked Questions

As structural closures in mature basins reach exhaustion, stratigraphic traps offer the most significant remaining resource potential. Specifically, experts believe these traps contain 50% of the undiscovered resources in the UK Continental Shelf. Consequently, the industry prioritises ‘advantaged barrels’—resources with low break-even costs—often found through infrastructure-led exploration (ILX).

Structural traps typically involve depth contour mapping of the reservoir top. In contrast, stratigraphic traps involve subtle facies changes or unconformities that often bypass detection on standard maps. Furthermore, the transition from a quality reservoir to a seal is rarely abrupt, which creates significant drilling risk.

Historically, these traps were viewed as higher risk. However, recent evidence shows that success rates in certain plays now match or exceed those of structural traps. Indeed, in many mature basins, stratigraphic discoveries provide larger average discovery sizes because obvious structures have already been drilled.

Major firms now use AI for reservoir learning rather than just simple seismic visualisation. For instance, seismic foundation models (FMs) like PRISM use self-supervised learning on massive datasets to identify broad subsurface patterns. Additionally, these tools link with Large Language Models to answer complex geological questions directly from seismic volumes.

Late-life assets currently serve as platforms for Carbon Capture, Utilisation, and Storage (CCUS). Notably, the oil and gas sector manages 75% of global CCUS capacity. Repurposing existing pipelines for CO2 storage is a cost-effective alternative to new builds, supporting projects like Northern Endurance in the UK.

Operators face declining production, rising operating expenditures (OPEX), and heavy decommissioning liabilities. In environments like the UK North Sea, high marginal tax rates—currently at 78%—have halted new field approvals, forcing firms to focus on low-cost interventions and asset consolidation.

Well interventions slow natural decline and enhance efficiency at a lower cost than new drilling. Specifically, in 2024, UKCS interventions delivered 37.5 million boe of production. Furthermore, intervention costs fell to £9.60 per barrel, which ensures healthy profit margins during late-life management.

Digital technologies like AI-driven well planning, wireless downhole surveillance, and real-time monitoring significantly reduce non-productive time. For example, machine learning models help engineers predict pump failures before they happen, which extends the field life of aging assets.