Key Takeaways

- LNG contract management is essential as the industry faces a complex cycle with increasing supply, price volatility, and local market challenges.

- Malaysia’s role is evolving from being an LNG exporter to potentially a net LNG importer, impacting pricing and contract strategies.

- Effective LNG contract management must align international agreements with local regulations and operational realities.

- The 2026 supply wave may spur price reviews and renegotiations, requiring strong LNG contract management to navigate market changes.

- Training for Malaysian energy professionals should cover LNG contract management, pricing strategies, and operational integration for effective value protection.

A new LNG cycle is coming

LNG contract management is becoming a strategic capability for Malaysian energy professionals as the global LNG sector moves into a more complex commercial cycle. Supply growth, destination flexibility, price volatility, regulatory scrutiny and geopolitical disruption have changed how buyers, sellers and advisers manage exposure across oil-indexed contracts, hub-linked contracts, spot procurement and long-term portfolio positions.

The International Energy Agency’s Gas Market Report, Q1-2026 expects global LNG production to increase by more than 7%, or over 40 bcm, in 2026. North America is expected to account for more than 85% of that increase.

That supply wave could create opportunities for buyers. It may encourage price reviews, renegotiations, shorter review cycles and more interest in hybrid pricing structures. But it could also expose weaknesses in older contracts, especially where legacy oil-indexed formulas, rigid destination rights or unclear delivery obligations no longer fit the market.

This is where LNG contract management becomes more than administration. It becomes a strategic capability.

The International Gas Union reported that global LNG trade grew by 2.4% in 2024 to 411.24 million tonnes, connecting 22 exporting markets with 48 importing markets. As LNG trade expands, buyers and sellers are dealing with a more connected, more flexible and more legally sensitive market.

For Malaysia and wider Asia, the challenge is sharper. A larger LNG supply wave may create more room to negotiate value, but shipping disruption, sanctions, terminal access, foreign exchange exposure and domestic gas policy can still tighten supply suddenly. The question is no longer whether organisations understand LNG. The question is whether they can protect value when the contract is tested.

Malaysia’s LNG challenge is no longer only technical

Malaysia provides a useful example because it sits across several LNG roles at once. It remains an established LNG exporter, a domestic gas market manager, a regional energy player and an economy facing long-term energy security considerations.

The International Trade Administration has reported that Malaysia imported 3.3 million metric tonnes of LNG in 2024, up from 2.1 million tonnes in 2021. It also noted projections that Malaysia could become a net LNG importer within the next 10 to 20 years.

That transition changes the commercial pressure on Malaysian energy professionals. LNG is no longer only about export value or upstream capability. It is increasingly connected to import strategy, regasification access, domestic price recovery, downstream affordability and security of supply.

In Malaysia, commercial teams are caught between global LNG pricing and local market realities. A contract may be linked to Brent, Henry Hub, JKM or another market reference, while domestic costs, tariffs and recovery mechanisms may be shaped by Malaysian regulation and Ringgit (MYR) budgeting realities. When LNG costs are effectively exposed to US dollar (USD) pricing, MYR volatility can become a real commercial issue for procurement, finance and downstream planning.

This is why LNG contract structuring and negotiation now matters beyond the legal team. The contract must work not only in the international LNG market, but also inside Malaysia’s evolving domestic gas framework.

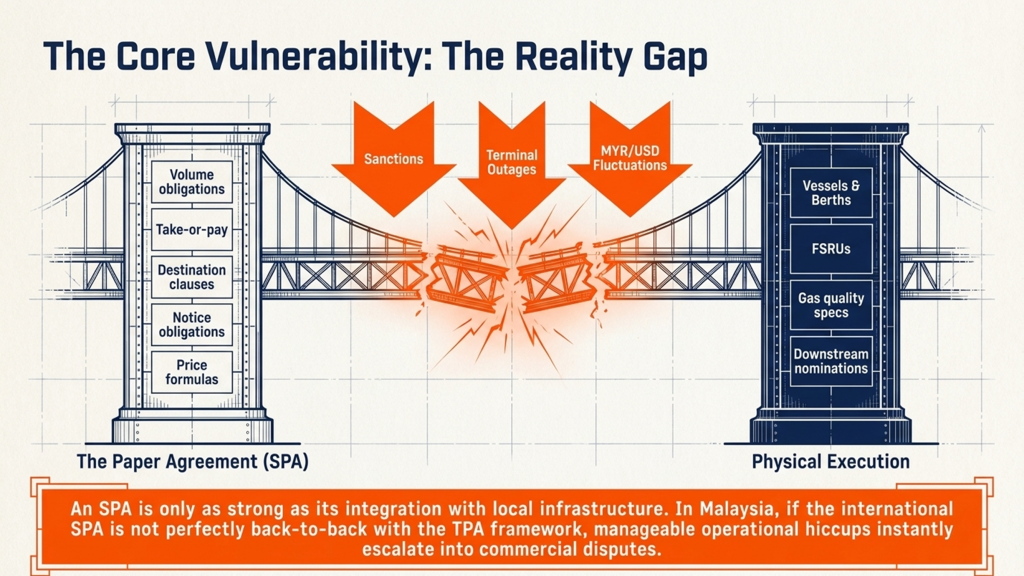

The real risk is the gap between the SPA and reality

Many organisations treat the LNG sale and purchase agreement, or SPA, as the centre of the commercial relationship. That is understandable, but incomplete.

The SPA may define price, delivery terms, volume obligations, scheduling rights, force majeure, sanctions, notices and remedies. Yet performance also depends on vessels, berths, storage tanks, regasification terminals, floating storage and regasification units, gas quality specifications, pipeline access, tariff structures and downstream nominations.

This creates a reality gap. The contract may look balanced on paper, but behave very differently during a terminal outage, vessel delay, sanctions event, price spike, currency movement or gas quality dispute.

For Malaysian professionals, the gap can be even more complex because the international LNG contract must align with local Third-Party Access requirements, terminal usage arrangements and network rules. If the SPA is not properly back-to-back with the regasification terminal usage agreement and the relevant network code, a manageable operational issue can become a commercial dispute.

Malaysia’s Third-Party Access framework is central to this discussion. Suruhanjaya Tenaga’s TPA materials refer to the Gas Supply Act 1993, Gas Supply Regulations 1997, Gas Supply (Amendment) Act 2016 and TPA codes for regasification terminals, transmission pipelines and distribution pipelines.

This means LNG contract management in Malaysia is no longer only about cargoes and price formulas. It is also about capacity rights, gas quality, balancing obligations, tariff exposure, gas transmission pipeline engineering and operational alignment between international and domestic arrangements.

An LNG SPA only protects value when it is aligned with real-world execution — from terminals and vessels to sanctions, gas quality and downstream obligations.

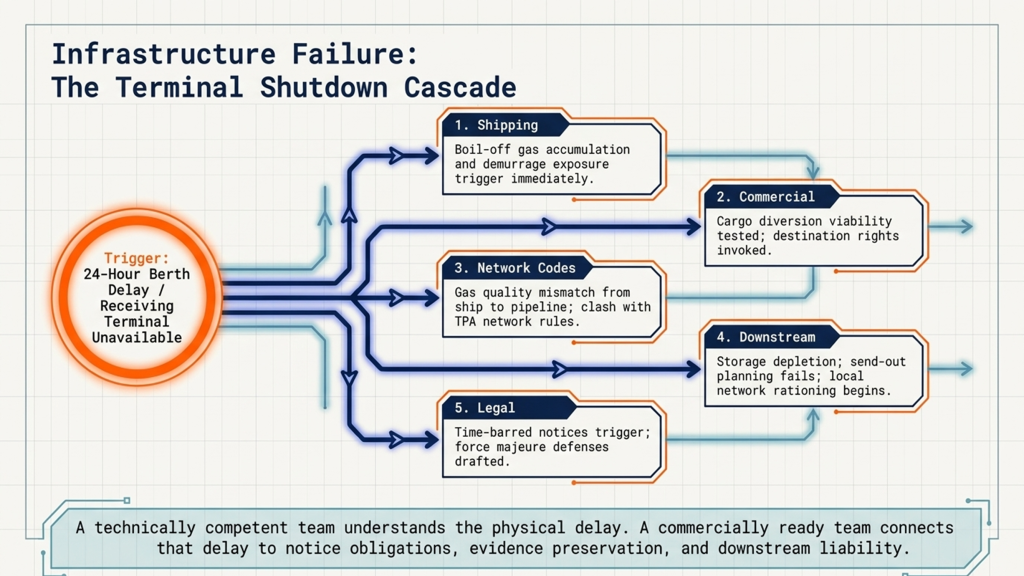

A practical test: what happens if the terminal shuts down?

A practical way to assess LNG commercial readiness is to ask how the organisation would respond if a key receiving terminal became unavailable at short notice.

In that moment, the team cannot afford to treat the SPA, the terminal agreement and the network rules as separate documents. It needs to understand how they work together. Who carries boil-off and demurrage exposure? Is force majeure relief available? Does the event genuinely prevent performance, or does it merely make performance more expensive? Can the cargo be diverted? Are gas quality specifications consistent from ship to pipeline? Do sanctions, insurance, vessel ownership, flag-state restrictions or port access affect the cargo?

This is where commercial judgement becomes visible. A technically competent team may understand LNG operations, but a commercially ready team can connect those operations to notice obligations, time-bar provisions, evidence preservation, pricing exposure, regulatory requirements and dispute prevention.

The same issue applies to shipping. For Malaysia and Southeast Asia, the Strait of Malacca is not just a map reference. It is a major strategic route for energy trade and LNG flows into East and Southeast Asia.

That matters because LNG commercial risk is not limited to the cargo price. It includes the route, vessel availability, port access, freight exposure, marine insurance, LNG charterparty management, destination rights and the ability to deliver gas into the local network when it is needed.

A terminal disruption can quickly cascade into shipping, commercial, network, downstream and legal exposure if contracts are not managed as one connected system.

Force majeure is not the same as commercial hardship

The next LNG cycle may bring more price reviews and more disputes. One reason is that difficult market conditions often expose misunderstandings about force majeure.

Force majeure may become relevant where performance is prevented or materially obstructed by events beyond a party’s control, depending on the wording of the contract and the governing law. But market volatility, freight cost increases or price spikes will not automatically excuse performance. If a cargo remains physically and legally deliverable but has become more expensive to ship, that is often a commercial risk rather than a legal excuse.

This distinction is especially important in LNG because disruption can sit across several layers at once. A shipping route may become riskier. Freight may become more expensive. Insurance may become harder to obtain. A terminal may be constrained. A downstream pipeline may have limited flexibility. None of these facts automatically answers the legal question.

The practical question is not simply, “Has something gone wrong?” It is, “Does this event trigger a contractual right, a notice obligation, a suspension right, a mitigation duty, or merely a more expensive performance obligation?”

That is why LNG contract management must include legal, commercial and operational judgement.

Sanctions clauses are no longer boilerplate

Sanctions risk has become a non-negotiable part of LNG contract management. Modern LNG SPAs increasingly treat sanctions, export controls and compliance with laws as active operational risks rather than standard back-end legal wording.

Commercial teams should not monitor only the named counterparty. They may also need to consider the vessel owner, charterer, technical manager, insurer, bank, flag state, port, terminal, cargo origin, cargo destination and any entities involved in payment flows.

A transaction that appears commercially sound can still create compliance exposure if one part of the delivery chain becomes restricted. In some contracts, a sanctions or compliance event may trigger suspension, alternative performance obligations, cargo substitution, payment restrictions or termination rights.

For Malaysian and Asian LNG professionals, sanctions awareness should therefore be embedded into scheduling, shipping, credit, procurement and contract administration. It should not be left only to legal review at the point of contract signing.

Contract structure decides where the pain lands

LNG contract structuring and negotiation determine where risk sits before the disruption happens.

The distinction between Free on Board (FOB) and Delivered Ex Ship (DES) remains central. Under FOB terms, the buyer usually controls shipping and may have more ability to optimise cargo destination, subject to the contract. Under DES terms, the seller generally retains greater responsibility for delivery to the receiving terminal.

| Contract area | FOB risk profile | DES risk profile |

|---|---|---|

| Shipping control | Buyer manages vessel scheduling and freight exposure | Seller manages delivery logistics |

| Destination flexibility | Buyer may gain greater diversion optionality | Seller may retain more routing control |

| Demurrage and laytime | Buyer carries more shipping execution risk | Seller carries more delivery execution risk |

| Portfolio optimisation | Buyer may have stronger flexibility if rights are well drafted | Buyer may have more limited optionality |

| Operational disruption | Buyer coordinates vessel and receiving arrangements | Seller manages delivery performance |

However, delivery terms form only one layer. Take-or-pay, annual contract quantities, downward quantity tolerance, make-up rights, quality specifications, sanctions clauses, credit support, price review mechanisms and notice provisions can all become commercially material.

A clause that appears balanced during negotiation may behave very differently during a supply interruption, terminal outage, MYR/USD movement or regional price spike. Strong LNG contract management therefore starts before signature, because poorly structured clauses often become operational problems during delivery, scheduling or dispute resolution.

This is why professionals working on Natural Gas & LNG Sales Agreements need more than a legal understanding of contract language. They need to understand how commercial clauses interact with shipping, trading, financing, terminal operations, fiscal assumptions and downstream market requirements.

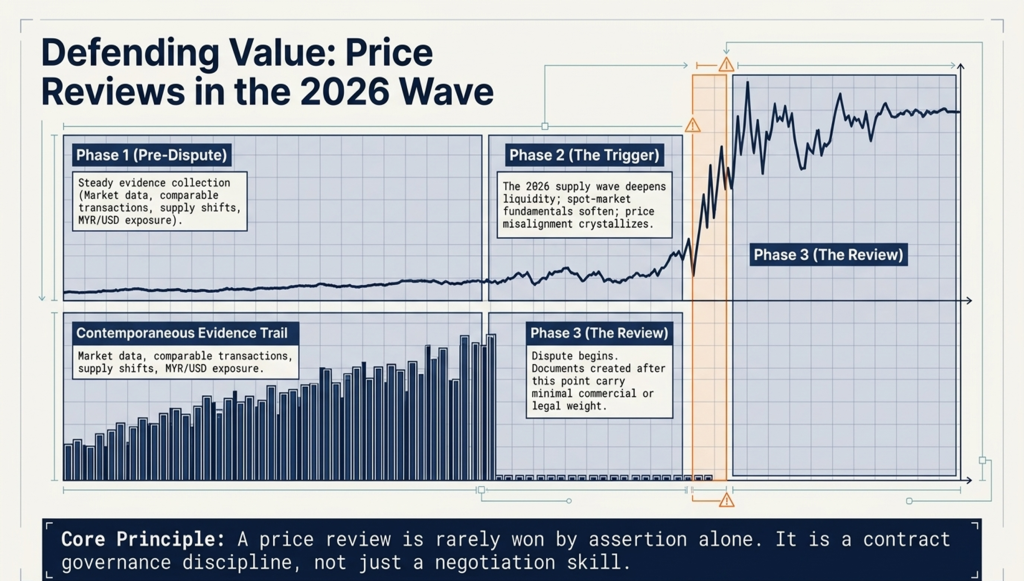

Price review is where the 2026 supply wave may bite

The 2026 LNG supply wave may be the most important commercial test for legacy LNG contracts.

If new supply deepens liquidity and softens spot-market fundamentals, buyers may seek price reviews, shorter review cycles or hybrid pricing structures. Sellers may resist formula changes where project financing depends on long-term revenue certainty.

For Malaysia, this is not only a trading issue. As the country moves toward greater LNG import reliance, commercial teams may have to manage the tension between global Brent, JKM or Henry Hub volatility and domestic price-smoothing or affordability considerations. Understanding how to structure price review clauses is therefore not only a legal task. It is part of energy security planning.

Price review clauses require careful governance. They are often among the most sensitive and contentious provisions in long-term LNG contracts because they can affect the economic balance of the entire transaction.

A price review is rarely won by assertion alone. Commercial teams should maintain a contemporaneous evidence trail from the moment a pricing misalignment is suspected. This may include market data, comparable transactions, index movement, regional supply-demand changes, shipping cost changes, MYR/USD exposure, internal pricing analysis, board papers, negotiation records and correspondence with counterparties.

The timing of this evidence matters. Documents created only after a dispute has crystallised may carry less commercial and legal weight than records maintained consistently over time. For that reason, price review capability is not just a negotiation skill. It is a contract governance discipline.

This is also where LNG markets, pricing, trading and risk management become directly relevant to contract governance. A team that understands trading exposure, hedging, freight economics and contract arbitrage is better equipped to decide whether a pricing issue is temporary volatility or evidence of a deeper market shift.

In the 2026 LNG supply wave, successful price reviews will depend on disciplined evidence, market data and contract governance — not negotiation pressure alone.

LNG shipping and terminal economics can change the contract outcome

LNG differs commercially from pipeline gas because shipping and terminal constraints sit directly inside the value chain. The contract may define obligations, but the vessel, berth, storage tank, floating LNG terminal, regasification unit, send-out system and transmission network determine whether parties can execute those obligations efficiently.

LNG shipping, trading and investment decisions therefore affect contract value. Freight costs, vessel availability, boil-off management, laytime, demurrage, heel requirements, LNG bunker requirements, diversion rights and charterparty terms can materially change cargo economics.

A 24-hour berth delay can create consequences beyond vessel cost. It can affect downstream nominations, storage availability, send-out planning, buyer claims and future scheduling flexibility. Shipping literacy is therefore not a niche marine skill. It forms part of LNG commercial competence.

Port pricing and tariff charging for oil and gas terminals also matter. Terminal access, port dues, regasification charges, capacity rights and tariff structures influence the landed cost of LNG. A cargo that appears competitive on commodity price may lose value after shipping, terminal and downstream charges.

Further downstream, gas transmission pipeline engineering and gas distribution network rules affect how LNG imports translate into reliable market supply. Regasification capacity has limited value if downstream pipeline constraints restrict flexible send-out or increase congestion during peak demand.

The practical point is straightforward: LNG contract management cannot sit apart from physical infrastructure. Commercial decisions need to reflect marine, terminal, pipeline and distribution realities.

Commercial judgement is the survival skill

The answer to this more complex LNG market is not simply “better contracts.” Better contracts matter, but they are not enough.

Effective LNG contract structuring and negotiation rests on five connected capabilities.

The first is contractual elasticity. Teams need to understand how clauses behave under force majeure, sanctions, outages, commissioning delays, price volatility or logistics disruption. This includes knowing where the line sits between operational impossibility and unprofitable performance.

The second is operational interface. A berth delay, terminal outage, vessel constraint or send-out limitation can change contractual and financial exposure. The team needs to understand how operations translate into claims, notices and commercial decisions.

The third is financial exposure. LNG teams need to assess hub volatility, Brent-linked pricing, foreign exchange, freight, credit support and margin movement. For Malaysian teams, this includes understanding how USD-linked LNG exposure interacts with MYR budgeting and domestic cost recovery.

The fourth is strategic agility. Cargo diversion, portfolio optimisation, contract arbitrage, renegotiation and settlement may create value, but only if they are commercially viable and contractually permitted.

The fifth is evidentiary discipline. In a dispute, the party with the strongest contemporaneous records often has the stronger position. Commercial judgement therefore includes document retention, internal escalation and strict compliance with notice deadlines, including notices of readiness, force majeure notices, dispute notices and other time-barred communications.

These are not abstract pillars. They are survival tools for the moment the contract is tested.

Risk management extends beyond the LNG SPA

LNG contract management also overlaps with energy insurance and risk management, project economics, contract law and dispute resolution.

Commodity price movement is only one part of the risk picture. LNG risk can also include interruption risk, marine exposure, counterparty default, political risk, credit exposure, operational delay, regulatory change, off-spec gas, terminal congestion and contractual liability.

This is why commercial teams increasingly need to understand project economics, risk and decision analysis for oil and gas. The best contract position may not always be the best commercial decision if it damages supply security, creates unnecessary litigation risk or weakens long-term portfolio value.

Engineering, procurement, construction, installation and commissioning arrangements may also matter, especially for LNG terminals, regasification infrastructure, floating LNG units, gas processing facilities and pipeline systems. Delays in EPC, EPCIC or commissioning milestones can flow directly into LNG delivery obligations, terminal readiness and contractual exposure.

For this reason, LNG professionals benefit from a lifecycle view of contract law and risk mitigation in energy. Contract value is not protected only by drafting. It is protected by execution, claims management, evidence, governance and coordinated decision-making across legal, commercial, finance, shipping and operations teams.

Carbon clauses and AI are adding new layers of risk

LNG contract management is also being reshaped by emissions documentation and AI-enabled contract administration.

Buyers, sellers and financiers are paying closer attention to methane intensity, cargo-level greenhouse gas data, lifecycle emissions, Scope 3 emissions and the credibility of lower-emissions LNG claims. GIIGNL maintains an MRV and GHG Neutral LNG Framework for LNG-related greenhouse gas reporting.

Care is needed when using terms such as “green LNG,” “carbon-neutral LNG” or “lower-emissions LNG.” These terms should not be used as marketing claims unless the organisation has supporting evidence, approved methodology and appropriate legal review.

The EU’s Carbon Border Adjustment Mechanism does not initially apply directly to LNG. Its initial scope covers cement, iron and steel, aluminium, fertilisers, electricity and hydrogen. Even so, CBAM reinforces the broader direction of travel: embedded-carbon scrutiny is becoming more relevant across traded energy and industrial value chains.

AI adds another layer. AI tools can help track notice deadlines, flag renewal dates, identify inconsistencies and organise obligations. That support can reduce value leakage in LNG, where missed notices or weak documentation can create real commercial exposure.

However, AI cannot replace legal and commercial judgement. It cannot decide whether a price review deserves escalation, whether a force majeure position is likely to withstand challenge, or whether a disputed cargo delay calls for negotiation, settlement or arbitration.

There is also a confidentiality risk. LNG contracts often contain strict confidentiality, privilege and data-handling obligations. Uploading unredacted contracts, negotiation records, legal advice, pricing formulas, cargo schedules or counterparty correspondence into public AI tools may breach confidentiality obligations or compromise legal privilege.

Compliance-ready AI use therefore requires secure, private and properly governed environments.

LNG training course for Malaysian energy professionals

For Malaysian energy professionals, LNG capability now needs to go beyond market awareness. It should cover LNG contract management, LNG contract structuring and negotiation, natural gas and LNG sales agreements, LNG markets, pricing, trading and risk management, natural gas pricing, trading and hedging, LNG shipping and investment, terminal access, Third-Party Access obligations, sanctions risk, emissions documentation, MYR/USD exposure and lifecycle contract governance.

EnergyEdge offers LNG training courses designed to help commercial, legal, finance, procurement, shipping and operational teams understand how LNG contracts behave in real market conditions. The aim is to help professionals interpret contracts in context, manage pricing exposure, connect commercial terms with operational realities and protect value after signature.

For teams involved in Gas and LNG Contracts, Markets and Strategy, Advanced LNG Markets, Trading and Hedging, LNG Commercial and Operations Fundamentals, LNG Marine Terminal Loading Master responsibilities, Floating Liquefied Natural Gas (FLNG) projects, Gas Transmission Pipeline Engineering, or broader energy contract management, the core requirement is the same: professionals must be able to connect contract language with market movement, infrastructure constraints and operational reality.

Conclusion: The contract is only as strong as the team managing it

The LNG industry’s skills conversation should not stop at operational readiness or certification. Those issues remain important, but they represent only part of the capability picture.

The 2026 LNG supply wave may create opportunities for better pricing and more flexible contract terms. It may also expose contracts that were never designed for today’s volatility, sanctions environment, emissions scrutiny, TPA requirements or domestic affordability pressures.

For Malaysia, the stakes are practical. LNG sits at the intersection of import security, export value, domestic gas policy, Third-Party Access, MYR/USD exposure, terminal capacity, gas transmission infrastructure, LNG shipping, carbon reporting and long-term energy transition planning.

As LNG markets become more interconnected, flexible and exposed to volatility, the organisations that protect value will not simply be those with the best contracts. They will be those with the commercial judgement to manage those contracts when conditions change.

Frequently Asked Questions

LNG contract management means managing LNG sale and purchase agreements after signing. Teams use it to track delivery obligations, price review triggers, cargo nominations, notices, sanctions clauses, credit support, shipping exposure and dispute risks.

LNG contract management matters in Malaysia because the country must balance LNG exports, rising import needs, domestic gas policy and energy security. Malaysian teams also need to manage Third-Party Access, MYR/USD exposure, regasification access and downstream affordability.

LNG contract structuring sets the risk position before signing. It covers pricing, delivery terms, volume flexibility, destination rights, sanctions clauses and remedies. LNG contract management focuses on execution after signing. It covers notices, claims, price reviews, shipping coordination and contract governance.

The 2026 LNG supply wave may shift market power between buyers and sellers. More supply could lead to price reviews, renegotiations and more flexible pricing terms. Malaysian energy professionals need strong LNG contract management to respond to these changes.

Malaysia’s Third-Party Access framework links LNG contracts to local gas infrastructure rules. Commercial teams must align the LNG SPA with terminal access, pipeline access, gas quality, tariff and network requirements. If these documents do not align, operational issues can turn into commercial disputes.

Price review clauses allow parties to revisit pricing when market conditions change. They depend on the contract wording and supporting evidence. Commercial teams should keep market data, pricing records, correspondence and internal analysis before a dispute begins.

An LNG training course should cover LNG contract management, LNG contract structuring and negotiation, LNG pricing, trading and risk management. It should also cover shipping exposure, terminal access, Third-Party Access, sanctions risk, emissions documentation, MYR/USD exposure and lifecycle contract governance.