The oil and gas supply chain now faces pressure that goes well beyond procurement timing or material availability. Operational constraints, delivery risk and capability gaps are affecting project delivery, plant reliability, maintenance planning and workforce readiness across the sector. Activity remains firm in many parts of the market, but execution has become harder. Supplier capacity is uneven, lead times remain unstable in some categories, specialist labour is tighter, and regulatory demands continue to increase. As a result, operators, contractors and service companies are placing more weight on schedule confidence, coordination and delivery discipline.

That shift matters because supply-chain performance now influences decisions that once sat mainly in project or commercial teams. Upstream operators feel it in the move from concept to first production. Midstream businesses see the same pressure in the pace and sequencing of transport, compression and processing projects. Downstream operators face it through shutdowns, upgrades and maintenance campaigns that can either protect uptime or create avoidable disruption. Across the wider energy supply chain, delivery strength has become a competitive factor rather than a background support function.

For senior professionals, this is not only an operational issue. It is a business performance issue that reaches into project economics, asset reliability, workforce readiness and long-term competitiveness.

Why the oil and gas supply chain remains under strain

Current market conditions still support activity across oil and gas, especially where companies can extend existing infrastructure, sustain output at lower execution risk or improve value through selective upgrades. Even so, that activity now sits in a market with less spare capacity than many businesses expected. Long-lead equipment remains hard to predict in some categories. Contractor availability is tighter in selected trades and specialist roles. Vendor capacity also varies sharply by product, region and asset type, which makes planning less straightforward. Materials may still be available, yet late design decisions, weak forecasting, slow approvals and poor sequencing continue to disrupt outcomes.

The real problem is not only whether the market can supply what is needed. The bigger problem is whether companies can identify needs early enough, engage the right suppliers at the right time and protect the execution window. The oil and gas supply chain now has to absorb market volatility, internal delays and tighter execution windows at the same time.

Geopolitics, refining and trade are raising supply-chain pressure

Operational constraints are also being tested by a more volatile trading environment. Geopolitical bottlenecks remain a live risk, particularly in the Middle East. Regional instability has created severe supply shocks, increased uncertainty around shipping routes and forced rapid rerouting across global trade flows. In that environment, Russian oil is increasingly flowing towards China rather than India, while buyers across Asia adjust procurement patterns to reflect pricing, logistics and exposure to disruption. These are not abstract market shifts. They have direct implications for shipping availability, freight costs, delivery timing and inventory strategy.

The downstream picture is tighter than crude availability alone would suggest. Crude supply may be abundant, but global refinery capacity growth is still lagging product demand. That creates a bottleneck in the downstream segment, leaving refined-product markets more exposed than headline crude balances imply. Product margins can therefore remain firm even when crude prices soften. This changes the economics of outages, turnarounds and refinery reliability. When conversion capacity is tight, the cost of disruption rises across the chain.

Trade policy is adding another layer of complexity. New tariffs and non-tariff protectionism in 2026 are pushing many businesses towards a more regionalised supply-chain model. The older China+1 mindset is giving way to broader diversification, and in some cases to an anywhere-but-China sourcing logic, as firms try to reduce landed-cost spikes and geopolitical concentration risk. That does not eliminate dependency. It does, however, change vendor selection, contracting strategy and inventory positioning.

Ageing assets and frontier projects create a dual burden

Infrastructure condition compounds these pressures. Mature basins face rising costs to maintain ageing pipelines, platforms and processing assets, while greenfield projects in deepwater or remote frontiers continue to face delays because of shortages in specialised equipment, marine support and logistics capacity. The result is a dual burden: legacy assets require more capital to sustain, while new developments remain harder to execute on schedule.

Many of today’s supply-chain pressures start inside the organisation before they appear in the market. Engineering, procurement, operations, logistics, warehousing, finance and commercial teams all shape delivery outcomes. When those functions work in silos, schedule risk grows quickly and small delays become larger execution problems.

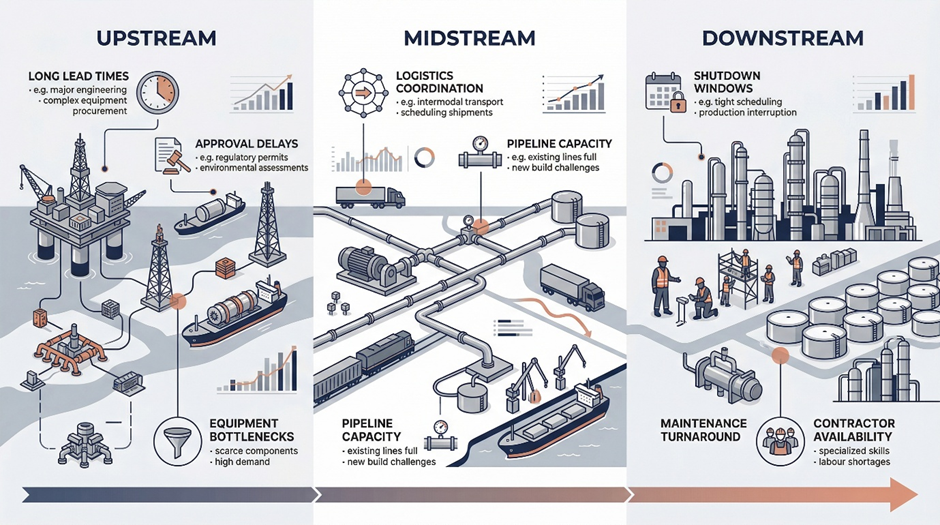

Structural risks across upstream, midstream and downstream

The most significant vulnerabilities differ across the value chain, but they point to the same issue: there is very little room for error.

Upstream: Complexity and interface risk

In upstream, companies often struggle with the combined effect of long-lead equipment, project complexity and tightly linked interfaces. Deepwater developments, subsea systems, compression packages and floating facilities all rely on close coordination between internal teams, suppliers and contractors. More novel designs usually create more interface risk, and more interface risk often leads to more schedule pressure.

That helps explain why repeatable concepts, phased developments and tie-backs to existing infrastructure have gained ground. In a tighter market, lower novelty is not just a technical preference. It is a delivery advantage. Fewer interfaces, more standardisation and a narrower vendor base can support better schedule control and reduce the chance of costly late-stage changes.

Midstream: Equipment bottlenecks and approval risk

Midstream projects face a different mix of pressure. Here, companies often struggle with the link between equipment lead times, construction sequencing and approval risk. Even when the strategic case is clear, project teams can lose time while waiting for rotating equipment, fabricated items or specialist components.

Those delays can alter the whole commercial picture. A project may remain sound in principle but become harder to deliver on the original timetable. Capital plans, contract strategies and customer expectations then come under pressure at the same time. In practical terms, physical execution can become a greater constraint than project intent.

Downstream: Tight windows and direct operational impact

Downstream businesses face pressure for a simpler reason: shutdown and turnaround windows are short, and the cost of delay is immediate. When refineries or processing plants work to narrow outage schedules, even small failures in planning, warehousing, supplier coordination or logistics can create major operational problems.

This is where procurement and logistics in oil and gas become highly visible. Late materials, poor traceability, incomplete workpacks or reactive sourcing decisions do not stay in the background. They affect uptime, restart quality, unit availability and plant performance very quickly.

Where pressure builds across upstream, midstream and downstream operations

Cost and schedule pressure now define delivery performance

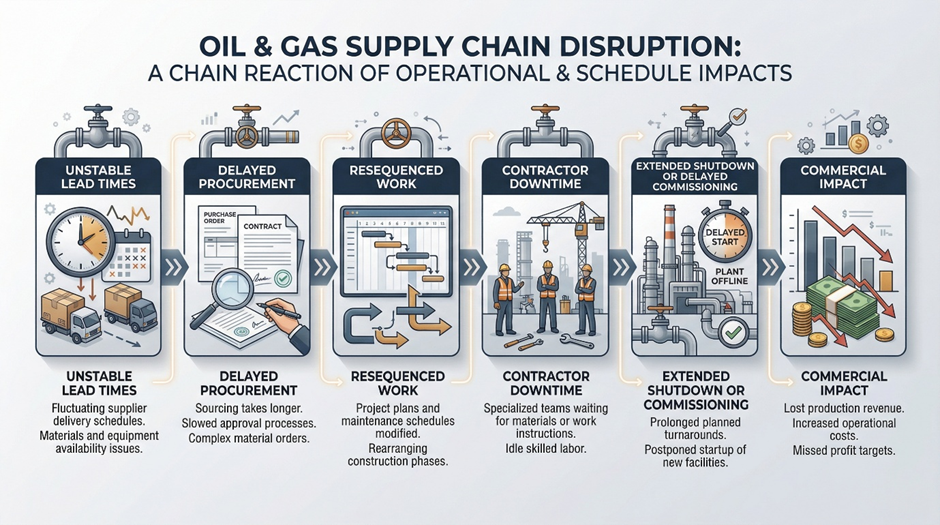

Many industry discussions still focus too heavily on inflation. Higher costs matter, but price alone does not explain the full problem. A more serious issue comes from the mix of price pressure, uncertain lead times and weak coordination. One late delivery on a critical item can trigger resequencing, contractor downtime, deferred commissioning, longer shutdowns or last-minute scope changes.

Each of those outcomes can damage performance more than the original price rise. Companies can sometimes absorb a higher purchase cost. They struggle far more when they cannot trust delivery dates, release decisions on time or complete work within a fixed operating window.

This is why schedule pressure now sits at the centre of operational performance. Operators have become more selective. Contractors show more caution when scope is unclear. Suppliers want better demand visibility before they commit scarce capacity. The market may still look active, but it now behaves with more care and less tolerance for uncertainty.

A wider downstream bottleneck adds to that pressure. While crude balances may appear manageable, refinery growth remains slower than product demand in many regions. That creates a mismatch between feedstock availability and conversion capacity. Product margins stay relatively high, outage risk becomes more expensive, and schedule performance carries more financial weight than it did in looser market conditions.

How a single supply delay can cascade into broader cost, schedule and execution pressure

Capability gaps behind supply-chain underperformance

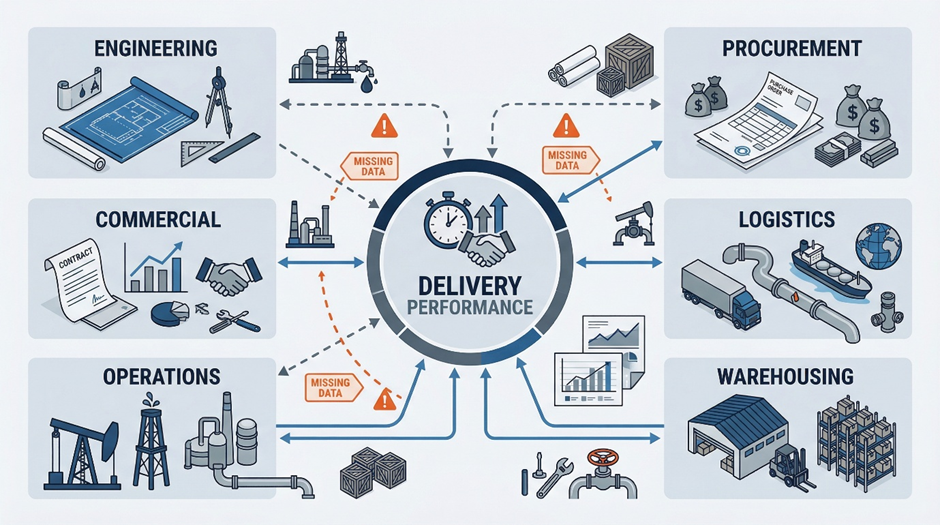

One of the most important changes in the sector is that many delivery failures no longer come only from external shortages. They come from internal capability gaps.

The weakest point in many organisations is not technical skill on its own. The real weakness often sits between functions. Engineering may release incomplete data. Procurement may approach the market too late. Operations may define needs after supply windows narrow. Logistics teams may lack timely visibility of changing priorities. Commercial teams may push contract terms that look efficient on paper but create delivery risk in practice.

These gaps explain why supply chains underperform even when suppliers exist and budgets are approved. They also explain why performance improvement often stalls when companies focus only on price, systems or headcount without fixing how teams work together. Many of the most persistent problems across the oil and gas supply chain now come from weak coordination, delayed decisions and fragmented ownership rather than from outright material scarcity alone.

Governance and digital maturity remain uneven

A broader governance gap is also becoming clearer. Legacy governance models were built for high-margin, high-risk hydrocarbon extraction. They are less well suited to diversified portfolios that now include lower-margin, utility-style assets such as renewables, hydrogen and emerging carbon-management activities. As businesses expand across old-world and new-world energy systems, governance has to manage different return profiles, different planning cycles and different operating logic. Many organisations have not yet fully adapted.

Digital execution maturity remains uneven as well. Many firms now have digital twins, predictive analytics platforms or AI-enabled maintenance tools. Yet the gap between digital deployment and digital trust is still material. In many organisations, planners and operations teams continue to rely on manual overrides because confidence in AI-led recommendations, data quality and workflow integration remains incomplete. That limits the predictive value of machine learning in maintenance, planning and logistics.

Workforce and data gaps are slowing response times

Workforce risk is tightening the constraint further. A large share of the technical workforce is approaching retirement, and the replacement challenge is not straightforward. The industry still needs experienced petroleum, maintenance and operations talent, but it increasingly also needs people who understand data, automation, carbon accounting and digital systems. The shortage is no longer only about headcount. It is about hybrid capability.

Data standardisation remains one of the least visible but most costly gaps. Fragmented data across upstream, midstream and downstream operations prevents real-time visibility of total value. That reduces responsiveness during disruptions, leaves capacity underused and slows decision-making when speed matters most. The result is not only inefficiency, but also weaker resilience.

That is why oil and gas training needs a more practical role. Many companies do not only need specialist technical training. They need stronger decision-making across planning, materials management, vendor qualification, demand forecasting, inventory control, contract administration and escalation. The same applies to supply chain training. Strong teams do not just buy well. They align technical needs with commercial choices, identify critical-path risk early and manage expediting, warehousing and operations with greater discipline.

For businesses facing delivery pressure, capability building is no longer separate from execution strategy. It now forms part of it.

Why coordination across engineering, procurement, logistics and operations now matters as much as supplier capacity

Regulation and technology are reshaping the oil and gas supply chain

Regulation now affects supply-chain design more directly than before. Rules linked to emissions, traceability, reporting and supplier accountability shape how businesses qualify vendors, manage documents and govern data. Compliance no longer sits at the edge of operations. It now reaches into day-to-day execution.

That creates extra pressure where procurement, operations and technical teams still work in disconnected ways. A fragmented model makes it harder to prove traceability, respond to reporting demands and maintain confidence in supplier information. The more complex the asset base and vendor network, the more important governance becomes.

Technology can help, but process discipline must come first. Digital tools can improve supplier visibility, materials tracking, procurement analytics and workpack control. They can speed up reporting and highlight risk earlier. Even so, software will not fix weak ownership, poor data quality or inconsistent specification control. Better visibility only matters when teams use it to make better decisions.

For that reason, technology investment should support a clearer operating model rather than compensate for a weak one. Companies that understand this distinction are more likely to improve both resilience and delivery performance across the oil and gas supply chain.

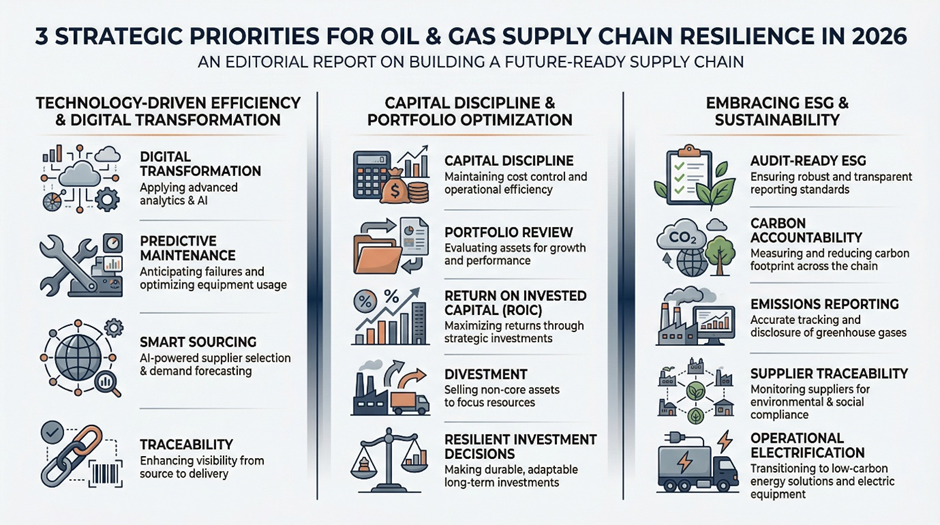

Strategic priorities for 2026

Several priorities now stand out across the sector, but in 2026 they are clustering around three broad pillars: deeper digital execution, tighter capital discipline and audit-ready decarbonisation.

A. Digital transformation and AI-driven total value

The first priority is moving beyond pilot programmes and connecting digital tools across the full asset and supply-chain lifecycle. The strategic goal is no longer simply to digitise a task. It is to connect planning, operations, maintenance and logistics tightly enough to act before failure, not after it.

Predictive maintenance now sits at the centre of that shift. The operational case is straightforward: when margins are tighter and downtime is costlier, pre-empting equipment failure is far more valuable than reacting after the event. Refineries and processing assets are increasingly using analytics to anticipate failures before they become expensive disruptions.

Smart sourcing is evolving in parallel. In some organisations, that now includes blockchain-enabled traceability, digital product passports and stronger digital provenance tools to improve visibility of origin, carbon footprint and compliance requirements. As regulatory expectations become more demanding, procurement decisions increasingly need to reflect both commercial needs and reporting requirements.

B. Capital discipline and portfolio review

The second priority is capital discipline. With Brent crude widely stress-tested around the $50 to $60 per barrel range in downside planning scenarios, the emphasis has shifted towards free cash flow, ROIC and balance-sheet resilience rather than aggressive growth. In practical terms, companies are asking harder questions about project timing, scope complexity and the real cost of execution risk.

That same pressure is driving portfolio review and divestment. Divestment is no longer only a balance-sheet action. It is increasingly part of how companies future-proof the portfolio by selling non-core, higher-carbon or structurally weaker assets. Portfolio quality now matters more than portfolio size.

C. Audit-ready ESG and decarbonisation

The third priority is turning sustainability from a reporting exercise into a control framework. Carbon accountability increasingly needs to be managed with the same level of rigour as financial data. That means clearer ownership, stronger documentation, better supplier traceability and control systems that can meet audit requirements linked to frameworks such as ISSB and CSRD.

This is beginning to influence field operations as well as reporting systems. Operational electrification is gaining attention where remote assets still depend heavily on diesel and face high fuel logistics costs. Replacing diesel generators at remote rigs with renewable microgrids or hybrid power systems offers a route to lower Scope 1 emissions while also reducing logistics exposure in off-grid environments.

Three priorities shaping resilience, capability and delivery performance in 2026

What this means for decision-makers

The industry has entered a period in which supply-chain quality will separate stronger performers from average ones. Not every asset or project faces the same constraints, and not every company will respond in the same way. Still, the direction is clear. Supply chains no longer sit in the background. They now shape project selection, maintenance performance and commercial confidence.

For senior decision-makers, the message is direct. Resilience depends as much on internal capability as on market availability. Businesses that improve planning discipline, procurement timing, logistics visibility and cross-functional coordination will stand in a better position to deliver consistently, even while capacity remains uneven, trade conditions stay volatile and regulatory pressure rises.

This is also where leadership priorities start to shift. Delivery performance no longer depends only on contracting strategy, cost control or engineering maturity. It also depends on whether the organisation has the capability to make timely decisions, manage interfaces well and build confidence across the supply base.

Conclusion

The oil and gas supply chain remains under pressure because the sector now operates with less tolerance for delay, less flexibility in specialist capacity and greater demands on coordination. These pressures now affect the oil and gas supply chain at every stage, from planning and procurement to maintenance, logistics and execution. The problem does not sit only in sourcing or logistics. It runs across planning, engineering, procurement, warehousing, maintenance and execution.

That is why the strongest response is not reactive expediting or isolated cost cutting. The better response is a disciplined operating model built on earlier visibility, stronger coordination and sharper workforce capability. In that environment, procurement and logistics in oil and gas become more than support functions, and oil and gas training becomes more than a separate learning activity. Both now shape whether organisations deliver safely, efficiently and with confidence across the wider energy supply chain.

For organisations reviewing gaps in planning, procurement, logistics and execution, the next phase is likely to place more weight on targeted oil and gas training and supply chain training that improve practical decision-making, not just narrow functional knowledge alone. As operational complexity rises, capability development is becoming part of delivery performance itself. That is especially true in a market where digital execution, capital discipline and audit-ready carbon accountability now sit alongside traditional engineering and procurement priorities rather than outside them.

Frequently Asked Questions

The main challenges include long-lead equipment, uneven supplier capacity, labour constraints, weak planning discipline, limited cross-functional coordination, trade volatility and growing regulatory complexity.

Procurement and logistics in oil and gas are becoming more difficult because delivery windows are tighter, specialist equipment is harder to schedule, internal approvals move more slowly in some organisations and supply risk now affects both cost and schedule.

Oil and gas training supports performance by improving planning quality, procurement discipline, materials management, logistics coordination and decision-making between functions that affect execution.

Supply chain training matters because the energy supply chain depends on close coordination between technical, commercial and operational teams. Stronger capability in these areas can improve resilience, visibility and delivery performance.

Common capability gaps include weak planning discipline, poor materials visibility, late procurement engagement, limited vendor management, inconsistent contract administration, low trust in digital systems and weak coordination between engineering, operations and supply chain teams.

Companies can improve resilience by identifying critical-path risks earlier, simplifying scope where possible, improving supplier visibility, strengthening planning and inventory processes, diversifying sourcing and building stronger cross-functional capability across operational and commercial teams.

The energy supply chain has become more connected, with project schedules, maintenance windows, regulatory requirements, trade conditions and procurement decisions affecting one another more directly. Engineering, procurement, logistics, operations and maintenance teams now need closer alignment to avoid delays and execution risk.